Portfolio & Dividends Update : 1st Half 2023

Time flies, and as we find ourselves in the midst of 2023, it is remarkable to reflect upon the passage of time and experience that has unfolded. I’m sure we all have different experiences in the 1st half of 2023 in terms of portfolio management and performance. For me, the last two quarters were like YOYO and my portfolio was performing well till March ( up by almost 11%) with the hope China “re-opening and recovery “But, as time passes, the strength of the recovery is getting weaker month by month and now everyone is hoping for more “ stimulus policies” to boost the economy, with declining economic indicators like retail sales, property sales, high unemployment among youth, slower export due to weak demand from developed countries, lower PPI and almost flat or zero CPI figure.

All this has

made my portfolio up and down huge, dropping to -2% at one point, and rebounding slightly to

4.68% now, with hopes of more policy support from the government.

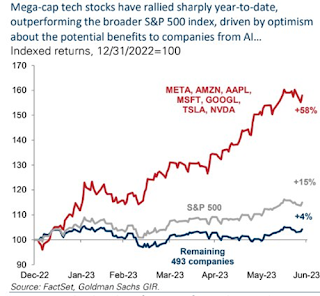

If you are

invested in the US or Japan market, congratulation !! you would have enjoyed more

than double digits return, +17.8% for S&P500, +24.1% for NIKKEI225, and even

higher for Nasdaq at +36.09% ( due to strong demand for Chips and so-called

mini-bubble from AI-related stocks).

The US

market is basically driven by tech mega-cap or AI-related stocks, even for

S&P500, the top 10 stocks accounted for almost 30% of its total value.

S&P

500 companies by weight <source: USA Today>

Since the S&P 500 is market cap weighted, meaning the

companies are included in proportion to their overall market size, larger

companies make up a greater portion of the index. This has become even more apparent

as the top 10 stocks in the

S&P 500 currently account for about 30% of the index.

I am not

sure if this so-called “mini-AI bubble” will continue or burst but I guess as

long as liquidity is still ample in the market, the party may continue.

To navigate

the AI stock bubble, it is crucial for investors to conduct thorough research, and evaluate a company's technology, business model, competitive landscape, and the

expertise of its management team. Additionally, understanding the regulatory

environment and the potential risks associated with AI technologies is

essential.

While there is significant promise in the field of AI, investors should be mindful of the potential for inflated valuations during periods of speculative hype. It is prudent to exercise caution, diversify investments, and adopt a long-term perspective when considering investing in AI stocks. By doing so, investors can avoid the pitfalls of a bubble and position themselves for sustainable growth and value creation in the AI industry.

We have seen a mixture of economic data for the US, while some economists predict a “soft landing

“ with mild and short recession, others are not so optimistic. The labor market remains strong coupled with lower

CPI/PPI data, market expects this Jul will be the last rate hike from FED or maybe another one in September.

As mentioned

before, interest rate hikes might have a delayed or lag effect on the economic front

and the market is very much “liquidity-driven”.

**A strong correlation between Nasdaq100 and Global CB liquidity since 2010 but there has been a breakdown since 2023. Will it last? or this time is different!

Some

economic indicators may look and remain strong, but the interest rate effect

may slowly show in some parts of economic activity and in some sectors already

feel the “tightening “of credit to some extent.

Based on the chart (research paper from FED), we can see that the negative effect on economic condition/Headwinds to GDP growth will only take effect 6 months after the first rate hike by FED in Mar 2022.

A New Index to Measure U.S. Financial

Conditions <Full paper here>

With a cautious note from the FED officer in fighting inflation and determination to bring

the inflation down to the 2% target, I think we should expect FED to hold the rate

for quite some time and even at the current level which is quite damaging to the economy and business environment. We may have more negative impacts from credit to companies or personal loan applications, to EPS from S&P500 in the coming quarter. We may see higher loan /credit card defaults as well as

companies’ files for bankruptcy.

Commercial Chapter 11 Filings Doubled Over Same Period Last Year <Source: sgyahoo.com.sg>

Americans are having a much harder time accessing credit. The rejection rate for loan applicants jumped to 21.8% in the 12 months through June, the highest level in 5 years: Fed data. The rejection rate for auto loans exceeded the application rate.

But as we

know, the market is “irrational” from time to time, even with “not so good “economic

data, the market will find ways and narratives to justify the next “bull run”. … as

always, liquidity plays an important role.

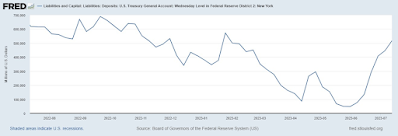

Even with

FED starting the QT in 2022 (which is a bit slow and affected by SVB event temporary), it still sits with more than 4+ Trillion QE $$ printed during the pandemic as compared to the pre-pandemic level.

Trillions

still sitting around the FEDs RRP account although some have already been channeled back

to Treasury’s TGA account (almost 500 billion increased in 1 month) after Congress

clear the debt ceiling issue.

Since

Government / Treasury is issuing short-term bills (T-Bill) to cover the huge

shortfall in the TGA accounts, the $$ mostly came from the FED RRP (where money

market funds temporarily park the $$ there) and some from bank reserves. By doing

this, the government will not affect the long-term bond rate, but of course, came with a huge cost in terms of short-term rate vs long-term rate. Although in the

short term, this may not affect the “liquidity “in the bond market eventually the government will need to swap this short-term bill with LT Bond. Selling the LT

Bond will help to push the LT bond rate and reduce the inverted yield curve but

at the expense of higher LT bond yield which is bad for economic growth.

But what to

do! with Government’s interest payment/expenses expected to increase to USD$

1 trillion in 2023, I don’t think they have many options ….

Well,

another issue/problem to consider will be the demand for such Long-Term Bond?

usually, 30-40% are bought by foreign entities / or the government. I think in the long

run, the biggest problem is still with the Bond Market …and this will have a huge impact in terms of demand for dollar and USD value. In fact, FED doesn’t (Fxxking) care

about how the stock market performs but I think they are more concerned about how

the bond market functions because anything that happens to the bond market may become a "systemic risk" which will affect the entire financial system. If you still

remember the “bond crisis” happened in the UK on September 2022 after the government

announced the mini-budget which also cause the removal of its finance minister

and the resignation of the Prime Minister subsequently.

UK’s

Bond Market Turmoil is a Wake-up Call for Pension Plans

< USD$1 Trillion and counting.......>

Well, of

course not all market rallies are just because of liquidity, the coming earnings or results announcement are

also important indicators, we will need a solid EPS to justify the current lofty

valuation, especially for those AI-related stocks.

Also, the ongoing

trade tensions with countries like China or the imposition of tariffs on

certain goods can have a huge impact and disrupt international trade flows,

increase costs for businesses, and potentially impact economic growth.

With the potential further tightening of IC / Chips equipment supply to China and

possible “retaliation” from China ( e.g on recent export control of certain chips

manufacturing material ), such “tic for tac” actions are bad for the global supply

chain and may have a massive impact on future economic growth.

Chip

companies, top US officials discuss China policy <Source:

Reuters.com>

U.S.

chip company executives met with top Biden administration officials on Monday

to discuss China policy, the State Department and sources said, as the most

powerful semiconductor lobby group urged a halt to more curbs under

consideration.

Earlier on Monday, the U.S.-based SIA called on the Biden administration

to "refrain from further restrictions" on chip sales to China and

urged the administration to allow "the industry to have continued access

to the China market, the world’s largest commercial market for commodity

semiconductors."

The Biden administration

is considering updating a

sweeping set of rules imposed in October to hobble China's chip industry and a

new executive order restricting some outbound investment.

Ok, enough

talking about the US market, now let's shift our attention back to SG or HKG market 😊

SG ST

Index :

As of today

(17th Jul 2023), STI closed almost flat and the same as at the beginning of

2023 at +0.08%.

STI is still

moving slightly below the long-term trend and doesn’t look cheap as during the crisis

but of course also not at the “bubble “level. I have not added any bank or stocks

which I own since the last update, except some REITs which I will explain

later.

But as I

mentioned before, if you are young and at the stage of “wealth accumulation “, this

could be a good chance to do DCA and deploy your capital slowly. For me, I will just

do nothing, keep calm, and collect dividends as usual. 😊

STI Top

10 Best and Worst YTD Performance:

|

| <data source:www.sginvestor.io> |

FTSE SG

REIT Index:

The YTD

performance of FTSE SG REIT is also almost flat at +0.73% and the Index has

gone down by more than -15% since the first rate hike from FED in early 2022. Higher

interest rates will affect the DPU with higher borrowing costs unless the REIT is able to increase the RENT to offset such cost increase. Within the REITs, I think the performance will vary as some might be able to have better

rental revision than others with worse performance from US Office REITs. In

the long run, I still believe that REITs could be a good “hedge” against

inflation and of course, the recovery may not be even for all REITs, some may

take time to recover some may be able to enjoy better rental revision.

REIT Top 10 Best and Worst YTD Performance:

<data source:www.sginvestor.io>

I have added

some REITs recently by using or re-cycle my capital from selling my US Tech

stocks which I manage to make some profit.

I know REIT

may continue to look challenging with interest may stay high for quite some

time, the market is demanding a higher risk premium in this regard. The outlook for

SG REITs will depend on a variety of factors, including the economic climate, interest

rate, market conditions, and specific dynamics (supply/demand) within the

real estate sector and its sub-sector.

Again, I

would suggest one to deploy your capital slowly and with an appropriate position

sizing. I know some really feel “stressed” and "stretched" with their capital to be

used in recent EFR from a few of the REITs. I think we must understand the REIT's

characteristic that it has to pay out 90% of the income and will need to do E.F.R ( Equity Find Raising) from time to time if there is an opportunity to expand. If you are holding

more REITs in your portfolio, it would be wise to keep some war chest to meet

such requirements, alternatively, you may consider trimming down % of REITs in

your portfolio and diversifying into other sectors like banks/conglomerates,

especially for a retiree like Uncle.

HKG Hang Seng

Index:

Wall

Street banks cut China's growth forecast after dull second quarter

Data on Monday showed China’s economy

grew 6.3% in the second quarter on a year-on-year basis, accelerating from 4.5%

in the first three months of the year, but well below expectations of 7.3%, as

demand weakened at home and abroad.

“Market skepticism on

China’s growth outlook is on the rise,” said Morgan Stanley economists led by

Robin Xing.

I guess this

is the kind of news you will see in most financial news platforms after China

announced its 2nd quarter 2023 GDP. A struggling property market, lower

demand for retail sales, weak exports demand from developed countries, lower

credit or loan growth, high unemployment rate, etc …. Together with geopolitical

tension and conflict with Western countries/alliances, this is going to be a

big challenge for China which I think may not end soon as long as the US still

think that China is a threat to them and challenging its dominance as the only “Super Power” in this world.

As mentioned

earlier, most of China’s economic indicators also pointed toward weaker

economic growth and pressure on disinflation and deflation. The market expects

(or is still waiting) further policy support from the government and a stimulus

package to support certain industries.

Looking at

the last 5 years' performance on HS Index, I am

not sure how many investors still have hopes and confidence about this market and

as an investor, you really need to have a “huge stomach” for such prolonged and

severe downturns in this market. To invest in this market, you will need a much stronger conviction and “Risk Tolerance “.

Portfolio

& Dividend Update: 1st Half 2023

TTL

Dividend & Interest 2nd Qtr 2023 : $46,614.34

TTL

Dividend & Interest 1st Half 2023 : $88,811.86

YTD

(Including announced for 3rd Qtr) : $115,365.57

*TTL

dividend received in 1st HF 2023 is around -10% lesser than last

year. This is mainly due to a one-off special dividend in specie received from

BHP ($14,834.04) in 2022, without this, the total dividend will be around the

same as last year's same period.

|

YTD Portfolio

XIRR: 4.68%

*My YTD

portfolio returns outperform STI by +4.6%, FTSE SG REIT by

+4.5%, HS Index by +8.5% and FTSE100 by +5.3% but underperform S&P500 by

-13.1%

** Most of

my return is from dividends collected as the total portfolio value is almost flat,

can see from below that mixture of stock’s performance within my portfolio.

I have

decided to take profit on US Tech stocks as the stock price has gone up quite a bit

due to AI stock mania (or some called it mini-bubble). As highlighted earlier, the

market is irrational and stock price for AI-related stock may continue to increase,

but I am ok with it and would like to just divert it to some value /dividend stocks. I may come back to these Tech stocks again as

I am sure that these tech companies are still very important for future growth,

remember when I said this is a kind of “winners take all” environment.

Lastly,

allow uncle to “nag” and as a reminder to me as well, having a diversified

portfolio across different sectors and countries is important as the market may “rotate”

from region to region or industry to industry. Although do understand that

having a “concentrated portfolio” may reap very good returns if we "bet" it correctly, as mentioned, you need to have a stronger risk tolerance with that and for

me, I would rather have “moderate or mediocre” returns in exchange for a

"peace of mind ", as a retiree I need to be more conservative.

On a personal level, the passage of time in 2023 has carried us through moments of joy, sorrow, and personal growth. We have celebrated milestones, forged new connections, and bid farewell to chapters of our lives. As we navigate the remainder of 2023, let us carry with us the lessons of the past months. Let us appreciate the preciousness of the time we spend with each other’s, friends, and family.

May we

embrace the opportunities that lie before us, knowing that time waits for no

one and that it is within our power to shape the future.

Keep Calm! Keep Smiling! ….and

collect dividends.

Cheers !!

Till next update. 😊

STE

Top 50 Holdings:

51-74 Holdings:

Comments

Post a Comment