Portfolio & Dividend Update : 28 Dec 2024

2024 is about to end in a few days, it was a rollercoaster year of market swings like a yoyo—up one moment, down the next. My portfolio value also had the same fate with the value up by +23% at one time and down to -2% at another point, and ended up with +16.5% as of 28th Dec 2024. Volatility ruled as global uncertainties and shifting sentiments tested investors' ability in portfolio management. Yet, amidst the turbulence, opportunities emerged for value-seekers to capitalize on irrational market moves. Let’s dissect how these dynamics shaped my portfolio performance and strategy this year.

The Singapore Straits Times Index (STI) saw a mixed performance YTD 2024, reflecting the broader market volatility. Starting the year on a positive note, it faced sharp corrections mid-year due to global recession fears and geopolitical uncertainties. It recovered strongly in 2nd half ( up by almost +13.2%), ending with a gain of around 16.4% YTD with a strong performance from 3 Big Banks, contributing most of the gains in STI ( DBS :+ 43.4% / OCBC : +27.1% / UOB : 26.6%).

STI is sitting above the long-term trend line by 7.7% with the main contribution from Big 3 Banks, especially from DBS ( +43.4%) after the company announced the $3 Bil share buyback program.

Share buyback at current valuation is a bit debatable, depending on the investor's valuation perspective as PB was at a historical high ( around 1.7) but of course, if based on PE or Dividend yield's POV, it seems still acceptable. I personally prefer this to be done in a better valuation rather than now although the share buyback may improve the EPS to some extent ( but not much with current valuation ).

Whereas Singapore REITs struggled as rising interest rates and a cautious economic outlook weighed on valuations. Industrial and logistics REITs showed resilience, while retail and office segments lagged, pressured by higher vacancies and softer rental growth. FTSE S-REIT YTD was down by -11.7% but dividend yields remained attractive, offering some solace for income-focused investors amidst a challenging year. The market remains cautious about higher interest rates for a longer time given the latest meeting update/feedback from FED ( expected only two more rate cuts in 2025). But even at a long-term rate ( 10 YRs Bond) of 4% and with an equity premium of 3+%, those REITs with 7+% look quite attractive if the assets can generate better rental revision in coming quarters, especially logistics or retail REITs.

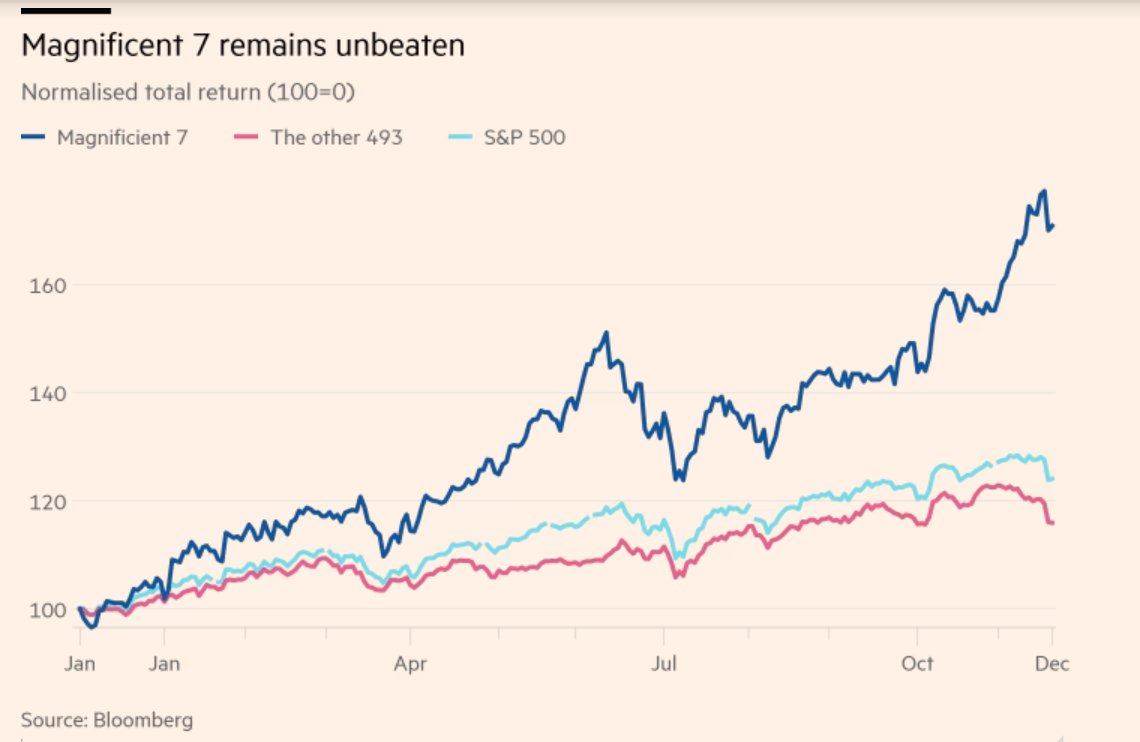

The U.S. stock market experienced a strong performance YTD in 2024, driven largely by a handful of mega-cap technology stocks, often referred to as the "Magnificent 7" – Apple, Microsoft, Amazon, Google (Alphabet), Meta (Facebook), Nvidia, and Tesla. These companies collectively accounted for a disproportionate share of the gains in major indices, particularly the S&P 500, reflecting an increasingly concentrated market environment.

Overview of Market Performance

The S&P 500 climbed by approximately 25.2% YTD, while the Nasdaq 100, heavily weighted toward technology, surged over 31.4%. However, the rally was far from broad-based. Sectors such as energy, financials, and consumer staples posted more subdued performances, with some lagging behind amid concerns about inflation, higher interest rates, and slower economic growth. The divergence between tech and the rest of the market highlighted the concentration risk.

Magnificent 7: Key Contributors

The Magnificent 7 collectively contributed over 70% of the S&P 500’s total return YTD. These tech giants benefited from:

- AI Boom: Nvidia emerged as a standout performer, driven by surging demand for its GPUs powering artificial intelligence (AI) applications. This enthusiasm for AI further bolstered Alphabet, Microsoft, and Meta, as these companies are heavily invested in AI development.

- Resilient Earnings: Despite economic uncertainty, these companies demonstrated robust revenue and earnings growth, underpinned by dominant market positions and diversified revenue streams.

- Investor Sentiment: Investors sought safety in these well-capitalized tech giants, perceiving them as better positioned to weather potential economic headwinds compared to smaller, more vulnerable firms.

Sector Concentration in the S&P 500

The Magnificent 7 now account for nearly 33% of the S&P 500’s market capitalization, marking one of the highest levels of concentration in decades. This has raised concerns about index fragility, as the index’s performance has become overly reliant on a small group of stocks. This concentration skews perceptions of market health, as the broader market (excluding these giants) has experienced more muted returns.

While the tech rally has lifted market averages, the concentration exposes investors to heightened risk if these companies face earnings disappointments or regulatory pressures. Moreover, reliance on a narrow segment of the market limits diversification benefits, posing challenges for passive index investors. Still, the tech sector’s innovation and leadership in AI continue to drive optimism for long-term growth.

As of December 2024, the forward price-to-earnings (P/E) ratios for the "Magnificent 7" tech giants are as follows:

| Company | Forward P/E Ratio |

|---|---|

| Alphabet | 23.1 |

| Meta | 27.4 |

| Microsoft | 34.0 |

| Amazon | 34.0 |

| Apple | 34.0 |

| Nvidia | 41.3 |

| Tesla | 87.9 |

Stock Markets is About Narrative / Stories and Capital Flow

Geopolitical tensions in 2024 have significantly influenced global capital flows, with investors seeking stability amid uncertainty. The United States, perceived as a safe haven, has attracted substantial investments, bolstering its stock markets. Conflicts and political instability in various regions have heightened risk perceptions, prompting investors to reallocate assets to more stable economies. Other than that, the robust performance of the U.S. economy, coupled with its political stability, has made it an attractive destination for capital seeking refuge from geopolitical risks.

Capital Inflows into the U.S. Market:

In 2024, U.S. equity funds have experienced notable inflows, reflecting this shift in investor sentiment. For instance, in the week leading up to December 25, U.S. equity funds saw net inflows of $20.56 billion, rebounding from significant net sales of $49.7 billion the previous week.

Additionally, November 2024 witnessed record-breaking activity in exchange-traded funds (ETFs), with inflows reaching $159 billion. In 2024, the U.S. financial markets experienced unprecedented capital inflows, particularly through exchange-traded funds (ETFs). ETFs attracted a record-breaking $1.6 trillion in new investments, surpassing previous annual records and bringing total ETF assets to over $15 trillion.

The United States is the envy of the world in terms of financial markets and economic performance.

Ruchir Sharma at The Financial Times outlines how this is impacting capital flows:

Global investors are committing more capital to a single country than ever before in modern history.

And the dollar, by some measures, trades at a higher value than at any time since the developed world abandoned fixed exchange rates 50 years ago.

The US now attracts more than 70 per cent of the flows into the $13tn global market for private investments, which include equity and credit.

America’s share of global stock markets is far greater than its 27 per cent share of the global economy.

There are reasons for the tidal wave of money pouring into the United States.......

Another factor attributed to this strong market performance is also caused by Stock Indexing. Index ETFs have significantly contributed to the concentration of U.S. stock markets around mega-cap companies, creating a "winner-takes-all" dynamic. These funds replicate the performance of market-cap-weighted indices like the S&P 500 and Nasdaq 100, which allocate greater weight to companies with higher market capitalizations.

How Index ETFs Drive Concentration

Market-Cap Weighting Bias: Market-cap indices inherently assign larger weights to the biggest companies. As ETFs track these indices, a significant portion of inflows disproportionately benefits the top-performing mega-caps, such as Apple, Microsoft, and Nvidia.

The popularity of Passive Investing: The rise of passive investing has funnelled trillions of dollars into index-tracking ETFs. This inflow amplifies the market caps of top constituents, creating a feedback loop where rising prices attract more flows, further inflating valuations.

Performance-Chasing Behavior: Investors favour ETFs due to their simplicity and strong historical returns, often driven by the top-performing stocks in the index. This behaviour further skews inflows toward dominant companies.

The butterfly effect, index funds, and the rise of megacaps

What goes up must come down was the mantra of small-cap investors for decades. Yet, over the last 10 to 20 years the largest companies have become larger and larger, outperforming small caps in the process. Some new research indicates that at least in part, this might not have been the result of mega caps being operationally superior to small caps but may be due to a butterfly effect triggered by index fund flows.

Index funds have long been prime suspects in the search for the reason why large companies have grown larger over time and why the US stock market, for example, is entirely dominated by a few mega-cap tech companies. I have always been suspicious of this argument because if you buy an index tracker, you buy each stock in the index in proportion to their market cap, so investors moving from active to passive funds should not influence the relative market cap of the stocks in an index.

Yes, index investors don’t correct mispricing of stocks because they don’t care about valuations, but the stock market remains dominated by active investors, and the market share of index trackers is in my view way too small to explain why megacap stocks trade at much higher valuations than most of the rest of the S&P 500, for example.

But when I read a paper by Hao Jiang, Dimitri Vayanos, and Lu Zheng I was surprised to see how flows into index funds create a butterfly effect among large-cap stocks.

While index ETFs democratize access to investing, their structural biases perpetuate market concentration and amplify risks for broader market stability.

Nobody can predict the market top and as long as there is continuous capital flow into the US market, the party may continue for many more years. One will need to be ready for high market volatility and stomach the risk of venturing into these markets.

|

| <Image Credit:Az Quotes> |

Before updating my Portfolio performance, allow me to share some photos taken during my last trip to China ( 稻城亚丁) in October 2024 😊

Daocheng Yading in Sichuan, China, is a hidden paradise, often called the "last Shangri-La." Surrounded by three sacred snow-capped mountains, its pristine alpine landscapes enchant with crystal-clear lakes, vibrant meadows, and stunning valleys. On this 10-day tour, we were really lucky that the weather was so nice that we were able to take such beautiful and scenic photos ![]()

![]() But as our tour guide mentioned, visiting DaoCheng Yading is like your "eyes will be like in heaven

But as our tour guide mentioned, visiting DaoCheng Yading is like your "eyes will be like in heaven ![]()

![]() , enjoying all these beautiful landscape but your body will be like in the hell

, enjoying all these beautiful landscape but your body will be like in the hell ![]() because of "altitude sickness" you will be facing while hiking at 4k m above sea-level... But with all these "paradise" like scenic, everything you suffered temporary was "worthwhile"..

because of "altitude sickness" you will be facing while hiking at 4k m above sea-level... But with all these "paradise" like scenic, everything you suffered temporary was "worthwhile"..![]()

![]()

![]()

我们很幸运,天气非常好,能有幸的见到三座神山。三座“神山”分别是仙乃日、央迈勇、夏诺多吉。北峰仙乃日,意为观世音菩萨,慈善安详,温馨平和,海拔6032米,为稻城第一高峰。南峰央迈勇,意为文殊菩萨,端庄娴静,冰清玉洁,海拔5958米。东峰夏诺多吉,意为金刚手菩萨,英俊刚烈,神采奕奕,海拔5958米。穿梭在海拔四千米以上,走动确是不易。

Portfolio & Dividend Update: 2024

YTD Portfolio Returns as of 28 Dec 2024: 16.46% ( XIRR)

Return since Inception (1998 ): 13.6% (XIRR)

Dividend Received in 2024: $ 189,480.82

* Total dividend received in 2024 is almost the same as 2023 (-0.3%), if taking into consideration of dividend in species from Tencent ( on Meituan) and Keppel Corp ( on K-Reit) which was valued at $5.8K, the dividend in 2024 will be slightly higher than 2023.

Portfolio Yield: 5.91%

Most of my portfolio returns were contributed by the HK market ( 9.34%) where the HK Hang Seng Index was up by +17.85% YTD and at one point it was up by +35.5% before retreating to its current level. My investment in the HK market finally gave a +ve return with this year's strong rebound in the Hang Seng Index. As of now, the overall HK portfolio XIRR is 2.1 % p.a ( with close to $145K in total profit), and if I exclude the Tech sectors ( which still sitting at -22% lost), my XIRR will increase to 5.5%, of course, not a great returns as compared to US markets, but with the current low valuation of HK market, I hope the situation may continue to improve with the pivoting of policies from central government.

In 2024, the Hong Kong stock market exhibited notable volatility, influenced significantly by China's policy decisions. On September 24, 2024, the Chinese government announced a comprehensive stimulus package aimed at invigorating the economy and equity markets.

This policy pivot marked a shift from risk control to growth support, signalling a more favourable environment for business expansion. In response to these measures, the HSI experienced a significant rally, with equities rising by around 25% since the policy announcement.

This surge was driven by renewed investor confidence in China's commitment to economic growth and stability. However, the initial optimism began to wane as investors recognized the limited scope of fiscal support accompanying the policy shift. Despite the government's pro-growth stance, concrete fiscal measures to bolster the economy were perceived as insufficient. This realization led to a retreat in the HSI from its post-announcement highs, as market participants adjusted their expectations in light of the modest fiscal interventions.

The lack of substantial fiscal support has raised concerns about the sustainability of the market's recovery. Analysts argue that while policy signals are important, tangible fiscal actions are crucial to sustaining economic momentum and investor confidence. Without robust fiscal measures, the market remains susceptible to volatility, as evidenced by the recent pullback from earlier gains.

In summary, the Hong Kong stock market's performance in 2024 has been closely tied to China's policy directions. The September policy pivot provided a temporary boost to equities; however, the absence of comprehensive fiscal support has led to a partial retracement of those gains, underscoring the need for concrete economic interventions to maintain market stability.

The only market that I encountered negative return was LSE which was mainly due to the lower price from BHP (down by -27.1%) which is the worst stock among my top 10 holdings and SHELL also down by -5.1%.

The U.S. market’s robust 2024 rally, fueled by tech giants and concentrated gains, raises valuation concerns. The S&P 500’s current forward P/E is significantly above historical averages, reflecting heightened expectations. Over-optimism could lead to corrections if earnings disappoint or economic conditions tighten.

Investors should adopt a balanced approach, focusing on risk management like having a more diversified and balanced portfolio that is not over-concentrated in high-growth sectors. Prioritize fundamentally strong, reasonably valued companies and stick to long-term goals, avoiding herd mentality.

While high returns are rewarding, prudent risk management ensures portfolio resilience during inevitable market pullbacks.

Thank you for sharing such a comprehensive and insightful year-end review of your portfolio and the broader market trends in 2024. Your detailed analysis highlights the significant volatility experienced throughout the year, driven by global uncertainties and shifting investor sentiments. It's particularly noteworthy how a concentrated group of mega-cap tech stocks propelled the US markets, underscoring the risks of over-reliance on a few key players.

ReplyDeleteYour observations on the Singapore Straits Times Index and the resilient performance of major banks like DBS, OCBC, and UOB provide valuable regional context, while the challenges faced by REITs emphasize the impact of rising interest rates. The discussion on the "Magnificent 7" and their disproportionate influence on the S&P 500 aptly illustrates the concentration risk and potential for market fragility.

Additionally, your insights into the biotech sector's volatility and the effects of index ETFs on market concentration offer a well-rounded perspective on different investment areas. Your emphasis on diversification and prudent risk management serves as a crucial reminder for investors navigating these turbulent times.

As we look ahead to 2025, your balanced approach of leveraging historical data and maintaining a disciplined investment strategy will undoubtedly aid in making informed decisions. Wishing you continued success and a prosperous year ahead!

Nice pictures!

ReplyDeleteFsmone has the YTD return of various ETFs listed in US, HK and SG. Can use it to see YTD returns of various index ETFs. Based on STI etf, STI returns is 22%. See https://secure.fundsupermart.com/fsmone/etf/factsheet/1232/SPDR-Straits-Times-Index-ETF

Your YTD returns for STI - 16.4% - may have excluded dividends.

Hi TNL, thanks for the comments, yes ,the STI index return I quoted is from Yahoo Finance and I suppose it exclude the dividend. For ETF returns, some might include the dividend/ reinvest.. need to find out more.👌😊

DeleteJust checked, fyi, based on Yahoo Finance, the ES3.SI YTD return is 16.56%, just slight difference with STI index data. Hope this clarify 👌😊

DeleteHi STE, Yahoo Finance YTD returns are based on the price levels between 1 Jan 2024 and now. It exclude dividends.

DeleteSTI ETF Price as at 1 Jan 2024: $3.31

STI ETF Price as at 28 Dec 2024: $3.858

3.858 / 3.31 = 1.1656 --> 16.56% returns

STI ETF provides $0.159 dividend in 2024 (source: https://www.dividends.sg/view/es3 )

STI ETF returns incl dividend = Price returns + Dividend Yield

= 16.56% + 0.159 / 3.31

= 16.56% + 4.8% = 21.4%.

Hope above clarifies

Hi TNL, Ah I C, yah , adding dividend will be around 21.4% .. thanks for the clarification. Very good return on STI actually 👌🙏 Cheers!

Delete