Beauty ( Value ) Is In The Eye Of The Beholder – Part 2

Stocks Valuation: Art or Science?

This is an “old age “ question that pondered all of us as an

investor and question we hear from time to time. For me, I think stocks

valuation is both a science and an art. We often hear that analysts are trying

to find the so-called ”intrinsic value”

of a stock or business and different model or methods of analysis would give a

different result of valuations, sometimes the variance could be huge.

|

| <Image Credit: Mishfitlife.com> |

Beauty (Value) Is In The Eye of The Beholder: Part 1

When comes to “valuation”, I think most of us will have his

name in our mind. Yes ! he is the so-called “ Dean of Valuation”,

Professor Aswath Damodaran, currently a Professor of Finance at

NYU’s Stern School of Business. He is one of the best-known experts on

valuation and is often the “go-to” source when analyst or reporters are trying

to understand the valuation of a hot new company.

<Introduction To Valuation by Prof Aswath Damodaran>

## This is part of a series of lecturer (25 sessions in

total ) by NYU Stern School Of Business. You may find the full series on

YouTube by this link.

https://www.youtube.com/watch?v=znmQ7oMiQrM&list=PLUkh9m2BorqnKWu0g5ZUps_CbQ-JGtbI9

Our friend, Kyith from Investmentmoats.com also

has written a great article about valuation in detail in his blog recently. You

may find the link as below :

What

I Learn About the Art of Valuation. <Source:InvestmentMoats.com>

When comes to valuation, everyone will have their own

“judgment “ or biases, and try to put a “figure” on their stocks target price.

For me, I think this is not “right or wrong”, as mentioned, the so-called

“target price” lies with our “ forecast or estimation” about the company’s future

revenue, cash flow, or growth. How

optimistic or pessimistic of our thinking about the sectors or industries will

affect the “intrinsic value” we derived from our estimation. We should always

just take the “target price “ from an analyst with “a pinch of salt “.

Is The Trend Your Friend?

“The trend is your friend” is one of the best-known

sayings, although this message is incomplete. The full version should be, “The trend is

your friend, until the end when it bends.” The trick with buying stock is to

to be patient through the small changes in price until you can identify the

point when the trend makes a change in direction or “bends.”

As I always mentioned in my blog, market moves in a cycle

and will “revert to mean “ in

the long run when there is overshoot from time to time, be it over-optimistic

or too pessimistic.

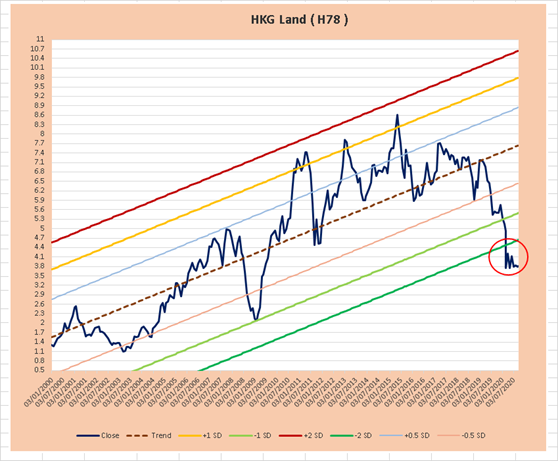

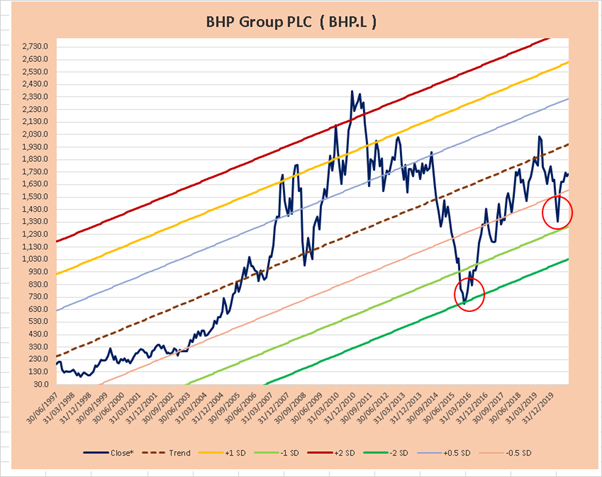

But how about at companies level? We have seen so many

companies trading at below -2SD level at this moment. Will these companies be

able to recover and their stock price reverting to mean eventually?

Of course, not all will recover or reverting to mean. Some

companies are facing real “structure or

fundamental change”, the challenge could be due to “ technology

disruption” (SPH), price war because of new competition (StarHub/Sing

Tel), economic cycles and cost factors (HPH, Keppel Corp,

SembCorp, Genting), internal restructuring ( HSBC, Sing Post)

etc. Some of these company may succeed to transform and recover eventually and

some may not, we will need to be extra careful in evaluating or doing a “recovery

play” kind of trading in such companies, of course, if you are betting it

right, the returns could be good.

Other than “fundamental change”, many companies are trading

below -2SD because

of a crisis or an economic downturn. If the fundamental of these companies still

solid and the current low stock price was mainly because of Covid-19 pandemic , the stock price may recover or rebound strongly once the pandemic is over.

Sectors like banking, hospitality, consumer staples will recover eventually and

of some may take much longer e.g Aviation

/ Cruise Lines etc. The probability of reverting to mean for such companies are

much higher than those with “fundamental challenges “. Most important is to

find a fundamentally solid company to invest and hold it for the long term,

patiently.

Final Thoughts

As I mentioned earlier, “Value is in the eye of the beholder”…every investor may have their own “thinking” or value about each

company they have invested. No right or wrong, some try to pick up the dividend

play and some trying to invest more on “growth stocks”, depending on your risk

appetite and investing time horizon. Even the “recovery play“ may turn out to

be a good one in your portfolio if you are lucky enough to “play “ it right.

Our friend, B ( from A Path to Forever

Financial Freedom) has written a very good summary of different “play” or categories of stocks

in our portfolio. You may find this interesting and see if you can breakdown

your portfolio into these 4 categories of stocks. :D

Allocating My Stock

Positions Based On These 4 Categories

Cheers !!

STE

Quote Of The Day :

“Numbers people believe that valuation should be about

numbers and that narratives/stories are distractions that bring in irrationalities

into investing. Narratives people believe that valuation

and investing are really about great stories and that it is the height of

hubris to try to estimate numbers when you face uncertainty.”

“Research in psychology point to an undeniable fact. Human beings respond

better to stories than to abstractions of numbers. This is true in business as

well, where storytelling often is much more effective at selling people on any

investment than the numbers that may be presented.”

By

Prof. Aswath Damodaran

Appendix: Regression Chart for selected companies.

Disclaimer:

The information contained within this blog is

provided for informational purposes only and is not intended to substitute for

obtaining professional financial advice as the writer is not a certified

financial adviser. You are responsible for your personal finances and should

not rely on this site or anyone else to make the final decision for you and

please do your own due diligent in using information from this blog.

Comments

Post a Comment