Portfolio & Dividend Update : 4th Aug 2024

Wow! Time flies as my last blog post has been almost 6 months. As we reach the midpoint of 2024, the stock market presents a mixed bag of opportunities and challenges. The landscape has evolved significantly since the beginning of the year, reflecting a complex interplay of economic indicators, geopolitical events, and corporate earnings. Investors are navigating a market that is both promising and unpredictable, shaped by ongoing adjustments in monetary policy, fluctuating inflation rates, and shifting global dynamics.

The first half of 2024 has seen notable volatility in the

stock market. After a strong start, equities have experienced fluctuations due

to a variety of factors. The market has been moving like a pendulum swing

since early of the year and we have started to see some pullback in the last

two weeks due to economic uncertainty. I guess the market is just trying to

find an excuse (weaker job data/ PMI / consumer confidence) to have such a correction,

which I think is quite common since it has been in an uptrend for quite some time,

whereas the S&P500 still enjoy a good +12.08% increase in YTD 2024

and 5 years return of +82.35%.

Growth stocks, in particular, have faced pressure as

interest rates continue to influence valuations even within the S&P500 you

may see the very high concentration of market cap with a few mega-cap stocks.

With such high concentration, again it is quite common to see a huge swing in the index,

this is a so-called “winner takes all market” and big will become

bigger with market-cap index design.

The “extraordinary “performance of the U.S. market is not just about earning, instead, is more on “liquidity “and capital flow after GFC and recent geopolitical events. Alongside the AI-driven optimism, a substantial influx of liquidity from global markets has bolstered U.S. equities. Central banks and financial institutions around the world have injected liquidity into the financial system through various means, such as lower interest rates and quantitative easing after GFC.

This global liquidity

has found its way into U.S. stocks, as investors seek stable and promising

returns amidst uncertainties in other regions. The flow of capital into the

U.S. market has amplified the positive momentum, contributing to the rise in stock

prices. Although the FED is doing the QT, there are still trillions of

dollars in excess liquidity created during the pandemic sitting on the FED’s

balance sheet. Other than that, there is also a huge budget deficit from the U.S.

government, while U.S. government debt plays a crucial role in stimulating

economic activity and supporting growth, the enormous $35 trillion debt

presents significant risks to global financial stability.

After the GFC, central banks worldwide have implemented

aggressive monetary policies, including low interest rates and quantitative

easing, to stimulate economic growth. The surge in global liquidity has

been a key driver of market volatility. Central banks' extensive

monetary stimulus has led to an influx of capital into financial markets,

creating an environment of heightened speculation and risk-taking.

In such a volatile environment, substantial drawdowns

(i.e., declines in asset prices) are not unusual, in fact it is quite common. Market

volatility driven by global liquidity and the potential for substantial

drawdowns are inherent features of the current financial environment.

The stock market is like a big “Casino”

now with huge volatility as you can see recently a -10/+10 % of trillion-dollar

big cap company like Nvidia is common. While one may continue to enjoy the ride/party,

these conditions can be challenging, employing effective strategies such as diversification,

risk management, and maintaining a long-term perspective can help

investors navigate the ups and downs. Remember the famous quote from a renowned

economist “The market can stay irrational longer than you can stay

solvent !”

Before I move on to update my portfolio, allow me to share

some photos taken during our trip to China ( 哈尔滨, 长白山天池) in early February 2024. 😊This holiday experience in Harbin and

Changbai Shan is a journey through stunning winter landscapes, unique cultural

experiences, and adventurous culinary delights. From the magic of Harbin's ice

festival and the invigorating thrill of eating ice cream in freezing

temperatures to the serene beauty of Changbai Shan’s natural wonders and the

indulgent relaxation of outdoor hot springs in minus 10 degrees during winter,

every moment of the trip is filled with wonder. One of the most adventurous

culinary experiences on this trip was tasting grilled silkworms. Known for

their rich, unique texture, silkworms are a delicacy in the region. 😊

Again, we are planning on our next 10 days trip to 稻城亚丁 in

October, hope to share more beautiful photos here.. cheers 😊

Portfolio & Dividend Update

As of mid-2024, the STI has demonstrated a mixed

performance. The index saw a peak in early March, driven by strong performance

in sectors such as financials and real estate. However, subsequent months

witnessed some correction and volatility. The STI’s performance has been

characterized by periods of sharp declines, followed by recoveries, reflecting

broader market uncertainties. As of today, banks are still holding well and can

see that all big 3 still have double-digit returns.

As for SG-REIT, the index saw a notable uptick in January and February, driven by positive market sentiment and strong earnings reports from several major REITs. However, as the year progressed, the index faced headwinds from rising interest rates and economic uncertainties. By mid-year, the sector showed signs of stabilization, with some REITs maintaining steady returns while others experienced more pronounced volatility.

Within the sectors, I still preferred Retail and Industrial/Logistics over Office / commercial REIT. Although we may continue to see an uptick in the cost of debt for some counters, the overall +ve rental reversion / DPU seems stabilized. We will not see the ZIRP any time soon even though FED is expecting to reduce the rate in September’s meeting as inflation might be a problem under the current geopolitical tension and supply chain “decoupling”.

As such, we shouldn’t expect a quick and fast rebound for SG-REIT but rather a slow recovery along with better rental reversion and DPU increase. Some REIT with high gearing may continue to face the increase in cost of debts, it may require better rental reversion to off set it slowly and eventually. I would considered REIT as a high leverage investment/ vehicle which is very sensitive to "interest rate " movement, hence the future FED rate trend will determine the value of REIT, although it may vary from sector to sector depending on supply/ demand ( future rental reversion).

In the first half of 2024, the Hang Seng Index displayed

significant volatility, characterized by periods of strong gains followed by

notable corrections. The index began the year with a positive trajectory, and it

gained almost +15% hitting a high of 19,636 in May, reflecting renewed

investor optimism and a rebound from previous lows. By mid-year, the index had

fluctuated considerably, with sharp declines attributed to a mix of

geopolitical tensions, and changes in monetary policy. Investor’s sentiment was dampened after the Third

Plenum of the 20th Central Committee meeting without a concrete

plan for solving the struggling housing issue or any significant stimulus

package to boost the economy (at least on domestic consumption).

The Third Plenary Session (aka Third Plenum), held in Jul 2024, is a significant event in China's political calendar, where key economic

policies and reforms are discussed and outlined. Traditionally, such meetings

can influence market sentiment, as investors look for signals regarding future

economic policies and stimulus measures.

The decline in the

Chinese stock market following the Third Plenary Session of the 20th Central

Committee can be attributed to several factors, including the lack of

anticipated stimulus measures, ongoing economic slowdown concerns, policy

uncertainty, and global market influences. The absence of substantial and

immediate support measures led to investor disappointment and market

corrections. Moving forward, the focus will likely remain on economic

performance indicators, potential policy adjustments, and global economic

conditions, as investors seek clarity and reassurances about China’s economic

trajectory.

Housing : The Mother

of All Problems

Housing is still the biggest issue for China’s economy and

the weakest link among the 三驾马车. China's housing

problem is multifaceted, encompassing high property prices, affordability

issues, excess inventory, and speculative investments resulting from a huge

stimulus package after GFC. The Chinese government has adopted it’s own way

and paths to solve this prolonged issue, a comprehensive approach tailored

to its unique socio-economic and political context. Through regulatory

measures, affordable housing programs, land use reforms, and financial

policies, China aims to stabilize the housing market, ensure socio-economic

stability, promote sustainable urbanization, and support long-term economic

growth.

The export seems doing well with a strong export

figure boosted by 新三样 and hope the strong export may continue to find

new markets and avenues.

新三样”出口首破万亿,释放出怎样的信号? <link>

As for the “Consumption”, without a huge stimulus package from government spending ( consumption), the diminishing wealth effect after the collapse of the housing market and a lacklustre stock market dampened the overall private consumption, can see the effect of drops in demand for luxury items in China in recent reports.

Boosting domestic consumption is a critical goal for China

as it seeks to transition from an investment-driven (property) growth model to

one driven by consumer spending. Enhancing domestic consumption can lead

to more sustainable economic growth and reduce reliance on property sectors and

exports. While the property sector may take time to heal, it is important to continue

to have high growth in exports and to boost domestic consumption. The

government will need to come out with real $$ and a concrete policy to address

this issue, or else everything will just be a 纸上谈兵.

As I mentioned in my previous blog post, investing in the HK/CHN

market is very challenging with various domestic issues and capital outflow

from foreign funds. Having a diversified portfolio strategy, focused

on income generation and fundamental strength, can help you navigate high

volatility and geopolitical uncertainty. Regular monitoring and rebalancing,

along with a mix of asset classes and geographies, will provide a stable

foundation for your retirement investments. Focus on companies ( 所谓轻市場,重公司)with strong

balance sheets, consistent earnings growth, and sustainable free cash flow with

competitive advantages.

Portfolio Update :

Portfolio XIRR :

YTD : +8.4%

Since Inception ( 1998 ) : +13.3%

My portfolio experiences significant and rapid changes in

value over short periods, is like a rollercoaster ride, resembling the intense

ups and downs from -ve 3% to +ve 11.8% and now decrease to +8.4% because of a big

swing in the HKG market. Overall, I am happy with this +8.4% return as I mentioned

earlier having realistic expectations on investment returns is crucial

in the current challenging market to avoid disappointment, manage risk

effectively, and make informed decisions. Understanding market volatility,

geopolitical tensions, and economic uncertainties helps investors stay

grounded, adapt strategies, and achieve long-term financial goals.

As a long-term investor, it's important to recognize that

recent double-digit growth in the S&P 500 over the past 15 years can create

a misleading perception of ease in investing. The post-Great Financial

Crisis (GFC) era saw significant government liquidity injections, driving

markets higher. This liquidity-driven environment can lead to recency

bias, where investors expect similar returns in the future,

underestimating potential risks and volatility. While the market has

performed well, long-term investing requires understanding that periods of high

growth are often followed by corrections or slower growth phases. A disciplined

approach, focusing on fundamentally strong companies and maintaining a diversified

portfolio, is essential. Recognizing the complexities and potential challenges

of investing helps manage expectations and build a resilient strategy, ensuring

sustainable growth and protecting against overconfidence driven

by recent market performance.

My portfolio is still very much skewed towards the HK/CHN

market with 52.9% of the allocation followed by SGX (30.3% ) and LSE (16%). As

highlighted earlier, the HK market has been challenging for the past 5 years

and I don’t have a crystal ball to predict what will happen next and am happy

to just hold on to my current holdings and wait while continue to receive my

dividends. 😊

You can see that property / REIT are still struggling under the

current high interest rate environment. (CLCT -25.3%, LINK REIT -23.5% (which I

added recently), ESR -14.1%).

Among the Top 10, BHP

has the worst performance (-21.8%), it dropped from 5th position previously

to nbr 8th now.

I reduced my holding in CNOOC / Shenzhen Int and switched

to non-oil counters as the % of Oil& Commodity has exceeded the Financial sector

in my portfolio. There is nothing wrong fundamentally with CNOOC as I just wanted to do some re-balancing of my portfolio. I added BAT / Vodafone/ Aviva/

M&G/ IG / Ashmore and Burberry from LSE and Perfect Medical

(1830)/ Stella Int Holding (1836)/ Fufeng Group (0546)/ Link REIT (0823)/

Bright Smart (1428) and Yankuang Energy (1711) from HKEX.

Dividend

Update :

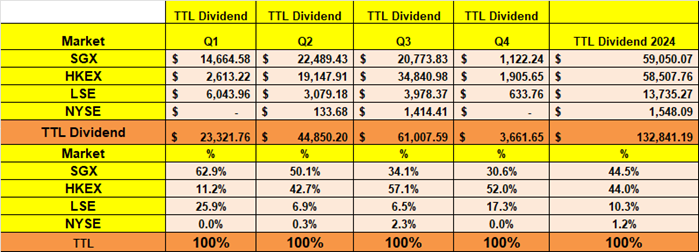

Total Dividend (collected & announced) : as of 4th

Aug 2023 = $132,841.19

3rd and 4th Qtr dividends should

increase further as more companies will announce their interim dividend, especially

stocks from HKEX and some from LSE/SGX.

As for the total dividend to be collected in 2024, I expect

it to be slightly lower as compared to 2023 mainly because in 2023 I received dividends

in specie from Keppel Corp (on SCM and K-Reit ), Tencent ( on Meituan) which is

valued at $21,395.16

The Power Of Compounding

Effect:

“Sedikit-sedikit Lama-lama Jadi Bukit”

This is not a chart to “hao-lian” on how much dividend I

have collected but to show "the power of compounding effect “over

a long period (26 years of investing).

Sometimes, we often hear people saying that dividend/income

investing is only for investors with a “big/substantial “amount of capital that

can generate a meaningful amount of passive income. I think this is wrong as you

can see, I was just collecting a few hundred dollar dividends in a year in my

early days of investing in the stock market and it has grown/compounded over a long

period of time.

Remember this chart I posted before, in the long run, there are parts of the equation in your portfolio, one is the total portfolio value which fluctuates according to market sentiment (in the short term) and grows with earnings ( in the long term), up and down subject to market sentiment and "regression to mean". The other part of the equation will be the dividend income you regularly receive from companies earnings/cash flow, this is the part that continues to grow for certain. 👌

Investing early, even with small amounts, offers

significant long-term benefits due to compound interest, reducing risk over

time, and leveraging market growth. Small, consistent investments establish

disciplined habits and make investing accessible. Focusing on income and

dividend-paying stocks provides regular income, reinvestment opportunities, and

stability from fundamentally strong companies.

Final thoughts:

Investing is a tough game, demanding patience

and a long-term view. It's not just about picking stocks; successful

investing requires disciplined portfolio management to mitigate risk. Emotions

and temperament play crucial roles in determining final returns. Market

fluctuations can provoke fear or greed, leading to poor decisions. Those who

stay focused on long-term goals and manage their portfolios wisely, balancing

risk and reward, are more likely to achieve sustained success. Emotional

control and a strategic approach are key to navigating the complexities of the

market and realizing consistent, favourable outcomes.

Investing is not a sprint but a marathon,

emphasizing the importance of a long-term perspective. In this race, you're

competing against yourself, not others. Achieving 1-2 years of good

returns doesn't guarantee future success; short-term performance can be

misleading. Sustainable investing requires a focus on the long run, where

consistent, disciplined strategies prevail. Market conditions fluctuate, and

what works in the short term might not be effective over decades. Long-term

investing demands patience, emotional control, and a commitment to continuous

learning and adaptation. By staying the course and focusing on

your personal financial goals, rather than comparing yourself to others, you

can build a resilient portfolio that grows steadily over time.

Learning and understanding financial history,

particularly regarding bubbles and bursts, is crucial for

informed investing. It helps investors recognize patterns of irrational

exuberance and market excesses, allowing them to avoid similar

mistakes. Historical knowledge provides insights into the causes and

consequences of past market crashes, fostering a more cautious and informed

approach to investing. This awareness aids in identifying warning signs, managing

risk, and making better decisions. Understanding "regression to the

mean" is vital, as it reminds investors that extreme market

conditions typically revert to average levels, emphasizing the importance of a

balanced, long-term strategy for sustainable growth.

Cheers ! Till next update 😊

STE

Top 50 Holdings

51-94 Holdings

Well done STE in this tough environment. Very impressive dividend. Agree need to have strong 'heart' and mind to experience the roller coaster situation. Thanks for your very detailed writing and generously penned down your thoughts on the way to do dividend investing with monitoring, some rhoughtful buy & sell to balance the pf.

ReplyDeleteHi ClassicMed, thanks for the comments and hope you will have a successful and Huat year in 2024!👍😊

DeleteThanks for your generous sharing and with all the breakdown. You might wonder if your sharing is useful for the community since no many responded, you are one of the solid one who sticks to your belief and I salute your investment style.

ReplyDeleteHi DC, thanks for the kind words and encouragement ! 🙏🙇that mean a lot for me to to continue my "sharing" and keep track on my portfolio performance as well 😊.Much appreciate your comments!

DeleteHi STE, With over 20 years of planning and hard work, impressive return for you! For me, I still haven’t found my perfect formula. I’m eager to learn from your blogs, though I know it will take some time to go through them all. If possible, could you share the total investment you made to achieve $160+ in dividends? Thank you!

ReplyDeleteHi SG Daddy, thanks for the comments n reading my blog 🙏 I think you need to look at the dividend amounts from whole investment process or journey person. It's being accumulated slowly with small amount initially. It grow slowly when you put in more capital or reinvest your dividend over the time. Also the amount will depends on your risk profile on what you expect of the yield on your portfolio. E.g if your portfolio are having higher %of yield ( which may come with higher risk) , like a 10% yield of portfolio vs 5%. Hope this clarify, btw, my current portfolio yield is around 5+% .🙏👌

DeleteHi STE, may I ask a question for a better knowledge ?

ReplyDeleteFrom your experience, on managing overall portfolio of dividend income stocks.

Recent years of fluctuations made it hard for me to swallow abit judging that my portfolio some years negative some years positive.

But I am still getting dividend income. Just that it i were to combine dividend returns with my portfolio capital returns. It will be a +- issue that comes up to no profit. Meaning capital loss yet got dividend coming.

Is this normal for this pathway ? Somehow if look at the spreadsheet feel like not making money if judging from this perspective.

How should I view it differently ? Or my spreadsheet need change ?

Hi Billy, thanks for reading my blog, yes, is normal to see negative in your portfolio return from time to time especially when certain sector in your portfolio is having some headwind and you are having high % in that sector. But if you read my previous post, it's quite normal as sector rotate due to business cyclicality. Up and down is normal but if you have a diversified portfolio, in the long run should be okay. As for the return, it would be better to look at it from total return perspective, i.e, your capital return or lose+ dividend received. You can put the dividend received into your xirr calculation. That will give you a better view or monitoring your overall portfolio returns. Hope this clarify.🙏

DeleteHi STE, I am new to your blog. Thank you for sharing your investment views. May I know which trading platform do you use and if there are custodian charges for holding so many foreign shares, thank you.

ReplyDeleteHi Jin_San, I am using Standard Chartered Bank and Poems ( Philip Securities) to buy these foreign shares. SCB doesn't have custodian charge for foreign holdings but for POEMS, there is custodian fees unless you meet certain criteria like trade xx time per month or hit certain AUM like $250k and above, it will be waived. For more in info,you may visit their website for more details. Hope this assist.🙏

Delete