2nd Quarter 2020 : Portfolio & Dividend Update

A

Shrinking “Panadol”!

I think this is the predicament for all of us as “income or dividend “ investors, seeing

our dividend received have a big "cut" or totally disappear like the case of “HSBC”.

We have noticed that most REITs start to be more prudent

in their latest distribution and conserving more cash during this Covid-19

pandemic. So far, banks like DBS still trying to maintain their quarterly

dividend but I guess at some point, they also would have to cut their dividend

if this crisis prolongs.

As investors, we will also need to be more “realistic “ in

our expectation, a 6-7% yield of stocks might become a thing of the past,

especially if we look at the “ultra-low “ interest rate environment.

Look at the interest rate for the latest SSB ( Singapore Saving

Bond ), for 10 years AAA bond is merely around 1%. Just guess how much you

will get from the bank’s FD rate? Suddenly, I felt more than happy and contented

with my money in CPF accounts which gave me an average of 3.3% for all three

accounts annually. (of course bear in mind that interest rate from CPF is also not guaranteed and subject to revise) :D

|

| image credit to seedly.sg |

This Month's Singapore Savings Bond (SSB): Interest Rates And How To Buy <source: seedly.sg>

Based on the past trend, an equity risk premium of 3-4% could be

reasonable and that would give us a stock (REITs) yield of around 4-5%, which I

am quite happy to have it. So, maybe we should not expect to get $0.33 /quarter of dividend from DBS from next onwards, if they maintain, it will be a

bonus for me.

In my previous blog post (

here ), I have mentioned that everything is “unprecedented “ undercurrent

situation and many traditional economic/financial model will be challenged and

some may need to be rewritten. Our working environment, consumption

behavioural, way of communication & interaction, cooperate, business model, will also see an “unprecedented” change and shift in the way we do things.

If you are planning for retirement, a traditional 4%

withdrawal rule may need to be adjusted as cash flow or returns from equity

will be much lesser, judging from the paradigm shift from what we are doing

now vs future.

This

Is A Time For Survival Not Yield

We begin to see more and more companies file for bankruptcy

especially from those industries badly hit and affected by this COVID 19 crisis

, ranging from Airline, Shale Oil, Retail and Hospitality to many more.

As investors, I think now the most important thing to

consider when making any investment decision will be “ survivorship” other than

cheap valuation like dividend yield or price to book value.

Nobody really knows how this pandemic may end and things

unfold, the situation may drag much longer than what we expected. Even developing

the vaccine is also not easy with so much uncertainty and unknown about this new virus, as it keeps mutating. Much initial research has shown that Covid-19 is

not just a virus causing “ respiratory problem”, but more than that. Scientist

and medical experts around the world are still in the early stage of trying to

understand this virus, not to mention the challenges they face in developing an effective

vaccine.

From blood clots to 'COVID toe':

Experts confounded by series of medical mysteries <source:straitstimes.com>

Hence, having a diversified portfolio is much more crucial

and important at this point of time, with so much uncertainty out there.

Quoted below from Howard Marks

on his latest Memo.<link to full Memo>

All We

Don’t Know

As

everyone knows, today we’re experiencing unprecedented (or at least highly

exceptional) developments in four areas: the pandemic, the economic

contraction, the oil price collapse and the Fed/government response. Thus

a number of considerations make the future particularly unpredictable these

days:

For investors, the future is

determined by thousands of factors, such as the internal workings of economies,

the participants’ psyches, exogenous events, governmental action, weather and

other forms of randomness. Thus the problem is enormously

multi-variate. Take the current situation with its four major components

(Covid-19, the economy, oil and Fed), and consider just one: the disease

·

It would be foolish, amid such uncertainty, to make overly

confident predictions about how the world economic order will look in five

years, or even five months.

Or maybe Voltaire said it best

250 years ago: Doubt is

not a pleasant condition, but certainty is absurd.

//Unquote //

Hence, it is important that not to be “overconfidence” to

have a very concentrated portfolio that betting in any particular stock or

industry. A more diversify or balance portfolio will be better undercurrent

“unprecedented “ situation. We should also pay extra attention to companies

with higher debts and weak cash flow. When a company stop to have any revenue

out of sudden, having high debts would kill. Also, at this moment, maybe is

better to look for companies which have “multiple sources” of income (e.g

conglomerate type of company) instead of relying on just single income or

business like airlines or hospitality.

So

, is dividend investing dead?

No, I don’t think so, the dividend will still continue

to play an important role in our valuation for any investment. In the long run,

those companies with strong and decent cash flow will still prevail and

triumph, except that if we can identify such companies under the current situation

where things will look so much different post-COVID-19.

More

Investing and Less Speculating

Yes, because of my overconfidence and stupidity, I lost -$185K in Eagle HT and this is my biggest

blunder after losing more than -$127k in Hyflux 6% CPS. But as I mentioned

before, Eagle HT is a very “speculative “

move for me, those buying it must with their eyes wide open because of weak and

unproven “sponsor”. With my belief and overconfidence in REITs that having a hard

asset, I keep averaging down till this became one my biggest position before I

cut lost at -65% in March when all REITs suddenly collapsed, even some blue-chip REITs also down by more than 30-40%. I also cut lost on ARA HT ( another

US Hospitality REIT ) with a loss of -$76K (-61%).

There are no excuses for my foolish on this, with weaker fundamental and

sponsor, COVID 19 had hastened the demise of Eagle HT with just one single

punch.

I have to learn how to invest from scratch, all over again…

I need an “Investing

101” !!

Dividend

& Portfolio Update :

** Revised as to exclude dividend from Eagle HT

Dividend 2nd

Qtr 2020 : $51,683.83

** Including dividend from HKEX = $20,134.63

TTL

Dividend 1st HF 2020 = $88,655.42

|

| image credit to : Izquotes.com |

This is the lowest amount to be received in 2nd

Qtr since 2016 as it normally ranged more than $60K.

With most of the REITs are conserving more cash, the DPU pay-out

been reduced from 20-70%. I think this will continue for quite some time and we

may expect even bank to trim their dividend in coming quarters.

As of 14th May 2020

STE Portfolio YTD Return : -24.5%

STI YTD: -21.75%

FTSE S-REIT (FSTAS 8670) : -19.81%

As of today, my portfolio under-performed STI by -2.75% ( - 7.44% including the dividend, base on ES3’s TTM dividend yield of 4.69% )

TTL Holding: 45

Top 10: 56.8%

Top 20 : 78.0%

STI Cumulative Return since 2007: 57.2%

FTSE S_REIT Cumulative Return since 2007: 130.8%

STE Cumulative return since 2007:170.9%

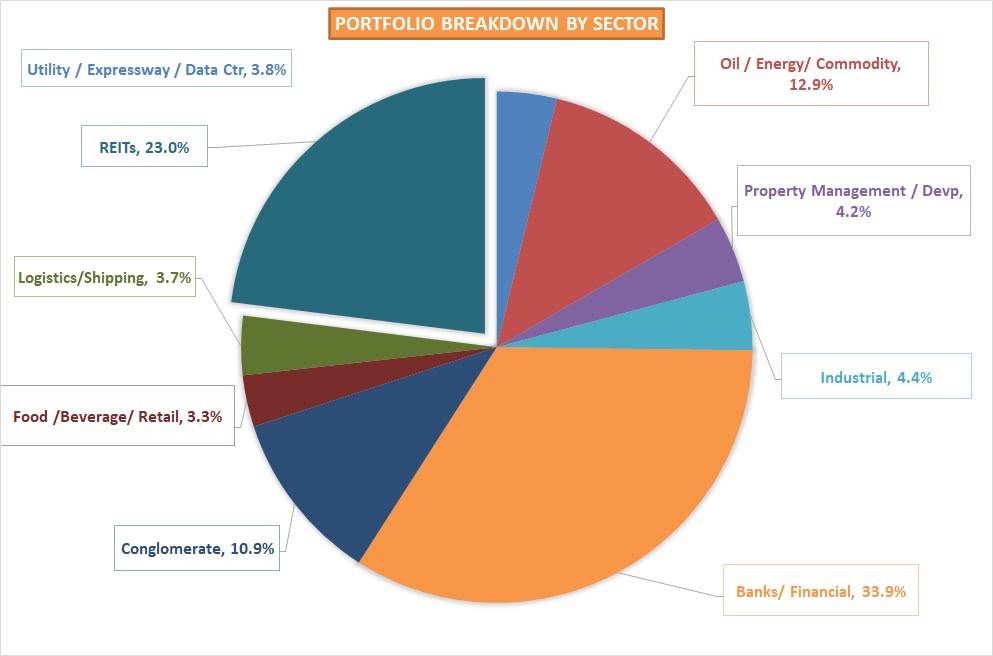

I have reduced my REIT holding from 44.7% to 23.0% and at

the same time increased my exposure to Bank/Finance to 33.9% ( from 14.8% ),

Conglomerate to 10.9% (from 7.5% ).

I also bought more HKG share in March/April, hence increased

my % of the portfolio in HKEX to 38.6% from 29.6% previously. Increased holding in BOC

HKG / CK Infrastructure and added CKH / CK Asset and Hang Seng Bank.

This is also the reason why there was a jump in my dividend to

be received from HKG in 2nd Qtr to $20,134 and $18,103 (already

announced in 3rd Qtr).

What is The

% of Your War-Chest?

Guess this is the most common question one will receive from

friends or peers among the investment community. I think the answer is very much

depending on your “risk tolerance “ and your forecast ( guesstimation ) about the market’s direction. Some may have a very optimistic forecast that fully vested

now and some may choose to have more war-chest and predicting that market may

collapse by another -50%. No right or wrong, as I mentioned before, I don’t

have the crystal ball to tell how the market will perform, it all depends on

your “risk tolerance “ and up to a level that allows you to sleep well at night.

“Quote Of The Day “

“In my younger

days I heard someone, I forgot who, remark “sell to the sleeping point”. This is a gem of the wisdom of the purest ray serene. When we

are worried it is because our subconscious mind is trying to telegraph us some

message of warning. The wisest course is to sell to the point where one stops

worrying ” Bernard

Baruch

Cheers !!

STE

Hey … you never tell us what is your % of war-chest now? Ops

!! is around 11.5% at this moment, but again, is very personal and depends on

your own situation …. :D

At least at this moment, I still stay the course and just

doing some portfolio rebalancing, but who knows, I may just turn pessimistic

suddenly and increase my war chest to 50% level… things remain very much

uncertain and COVID 19 keep mutating, we may need to move fast, sometimes.

Appendix:

Portfolio Holdings as of 14-May 2020 :

Hey Bro, sorry to hear the deep losses. I wanted to x you on EHT but who am I but a Kiasi and kiasu guy. Your remark on sleep well is very important as it has always been a key driving seat for me. I do miss some great rewards but I also avoid deep losses too. In the end is a fair game. But one thing very important which is health. I get to keep it. Cheers.

ReplyDeleteHi bro, thanks for the comments, indeed, good "expensive" lesson learned :(

DeleteYah, health is also important, now got money also can't go for holidays.. hahaha... take care bro.. cheers..:D

Same here..It was painful to see my portfolio dropping and my anticipated passive income cut by >20% during this CV crisis.. On the hindsight, I should not be too greedy to chase yield. After a whopping write off by selling some of my losers and valuating my EHT to 0, I have a realized loss of 70K.. Well, even Warren Buffet also lost 50 billion after cutting all his airline stocks.

ReplyDeleteHi GlobalPassiveIncome,

DeleteYah, market is really tough and uncertain, sometimes, we been "blinded" by high yield investing...need to be careful n always remind ourselves that ...no free lunch n good deal is sometimes too good to be true..

Stay safe and stay

healthy..

Cheers:D

Real life investors will lose relatively large sum of money at least once across market, economics, and industry cycles. Losing is part of the Game in investing or Money Game. After this big loss we may know ourselves better with our own data points and revise our investing strategies going forward.

ReplyDeleteHi Uncle CW8888, thanks for the advise and comments , yes, hope I would learn from this big mistake and be more prudent from now onwards. Yup, making loss is part and parcel of this so called "investing or money " game.. we would have to accept this but also learn from our mistake...

DeleteCheers !:D

Hi STE,

ReplyDeleteSometimes we win, sometimes we loss. Even Warren Buffett sold airlines that he just bought a while back. I think diversification and focus on risk & quality is important for the long run as we adjust our portfolio.

Hi Yaruzi,

DeleteThanks for the advise and comments , yes, we should focus on good quality company and always watch out for value trap and understand more on the risk / reward analysis of our investment. No free lunch though ...

Cheers ! :D

Hi STE,

ReplyDeleteyou are not alone. I cut loss on several shares (SIA, Sembcorp Marine, SingPost and Jumbo) in March too. Although the loss in terms of absolute amount is less than yours, the loss ranged from 25% to 72% loss for me. I also cut Hyflux at 60% loss too.

We will need to learn from these lessons. =)

Hi My Investment Machine,

DeleteThanks for the comments and sorry to know your losses on these counters , as what Uncle CW8888 mentioned , making loss is part and parcel of investing or money game, we will need to be more careful in our risk/reward analysis on each of our investment thesis ...of course , sometimes , value trap is hard to spot and we are blinded by the "higher yield "..

Yup... lessons learned and move on...

Cheers !! :D

Hi Bro.....

ReplyDeleteEveryone was and is experience the same.

I think no one will and was have a " only winning " depot.

Thinks will come better over time, thinks will change and the world and economy will have to learn how to live and survive with that Covid.

It's just that many changes and new chances we must search and look out for.

And maybe the one we not see yet and think yet will be the one provide us with our income next.

Cheers

Hi Unknow,

DeleteThanks for the comments and insights , Yes, , Covid 19 will bring new things on way we do business , communicate , shopping or even going to supermarket.

Is so much uncertain and unknown at this moment.

Stay home and stay safe !! Hope for better day post Covid 19 ..

Cheers :D

Hi STE,

ReplyDeleteSorry to hear on your Eagle's loss. I take a look at the chart, maybe you should consider yourself decisive and lucky to sell it before the counter get suspended. Anyway we all learn from mistakes, I also had purchased some stock in the past and within a very short time it got suspended. I never see light again. The company delisted without even paying a single cent.

Anyway, hopefully a few years from now, the market recovers and we can all gain from this Covid 19 market crash.

Cheers, and be safe.

Hi D,

DeleteThanks for the comments , Yes , lesson learned and move on... losing money is part and parcel of stock investing , the most important thing is learn from the mistake and try not to speculate on weak fundamental stocks...

Stay home and stay safe ...take care!

Cheers !! :D

Hi STE,

ReplyDeleteI just stumbled into your site and I'm pretty impressed with what you're doing. Also a word of thanks for sharing your journey, which is to many a very private thing.

I'm also retired after more than 20 years of trading derivatives in a major US bank and transitioned from a "specialist" to a generalist investor looking at almost all tradable markets.

When I first began, I built a portfolio which I cut into 2 parts, one a global growth portfolio and the other, a Singapore "low risk" portfolio comprising mainly of blue chips, and reits. The Singapore portfolio has a div yield of about 4.5 to 5%. The global portfolio is virtually no div and on average a negative EPS. The distribution of the portfolio was about 50-50 %.

Within a year, I reduced the Singapore portfolio by about 60% with the intent to reduce it further to zero eventually. Prior to the March "crash", it was 20% of my total portfolio and by today, it's a little less than 10%.

For this year, the Singapore part of my portfolio is down 20% which matched the STi which is down about 19.6%. Fortunately, my Global Portfolio is way up, and sufficient to more than compensate my local portfolio. My total portfolio returns is positive 12.8% so far this year. While I'm still long in total, I'm also fully hedge by shorting index futures as I think the current run up post crash is based on fantasy. There will be plenty of opportunites as the Covit19 story develops.

What I would like to say is that there are serious issues with the Singapore stock exchange. I list the following; some of which are controversial but that is fine.

1. Low level of transparency and difficulty in getting regular updates. Companies typically only provide information when they need to and tell you what they want to. An example is Eagle. Prior to their trading halt, the amount of information and discussion available is almost zero. You and I never stood a chance if we "value invested" in Eagle while seeking the juicy yield of 8%. After all, they do have big name hotels in the US at the time the US economy was booming in 2019.

2. A fairly thin market with low liquidity relative to other bourses. I would say participation and interest is low.

3. A lack of derivatives market like Options trading. This is important because it provides key data on where the smart money is. Public information like "open interest" and "volume" at various levels shows where are the key levels (strikes) and key dates (from the expiries).

4. No shortselling. Shortselling is controversial but it helps in the price discovery and is particularly useful when there's suspicion of fraud. A share like Eagle will be shorted prior to the bad news. At least, as you question about the sudden drop, you can make an informed decision to exit. A better example is Luckin Coffee which is Nasdaq listed and a GIC owned company. The writing was on the wall and I made money both ways riding it up, and shorting it from $35 to $5 before it was suspended. An observation and tracking of "short interest" gives a very good indication of what the short sellers are doing. It is much harder to trade from a short side and to be successful, you need a high level of experience and the investigative work is difficult and time, time consuming and sometimes expensive. And they make it public to whistleblow a potential problem. I take short sell reports very seriously. Watch the movie, "The Big Short" in Nextflix. Also google the firm Muddy Waters.

1/2

2/2

ReplyDelete5. Low quality of companies and management. Shareholders pressure are the biggest impetus for renewal and change. A high level of transparency demands that companies and directors account to shareholders with performance or there will be public demands for change. I see that many companies in Singapore are sloppily managed and the key management can pass the running of a company from generation to generation without sufficient accountability to shareholders and run in an incestous manner. It's a family affair with public money.

6. Low correlation between blue chips. The key business here are probably financial services and real estate. They are fairly good quality in good times if yield is our primary objective. We can split our funds up in a diversified portfolio and yet, one can make an argument that we are trading only one company, Singapore Inc. We look good in good times, and get severely exposed in bad times.

In summary, until we have a better process of price discovery, share investors here will always trade on "old news" and spend most of the time wondering what happened rather than understand what is happening real time. We drive forward with only a rear view mirror.

Best wishes in your journey ahead and I'm confident you will reach your investment goals long term, mostly based on our strong macro economic management. Based on the points I've raised, the path however could be rocky periodically.

Maybe a kopi one day to share war stories.

av

Hi av,

DeleteThanks for your "long " and valuable reply/comments. 真是受教了!!

Yes, as you pointed out, STI not really going anyway even after GFC since 2009, we don't have much growth or tech companies like FANG or even Alibaba / Tencent type of companies in STI. Also as you rightly mentioned, Singapore Inc may have passed it's "highest peak" during 70-90s where it managed to achieve some "miracle " with a stellar performance during that time.

Many so-called S-series blue chips ( or used to be blue chips ) (eg. SPH/SING Post/ SIA Eng/ ST ENG/SembCorp Marine / SembCorp Ind/ Star Hub / SING TEL/SMRT/SBS etc..) and even now SIA/SATS/ComfortDelgro ( these few might be due current Covid19 pandemic and kind of cyclical )...even if you look at Capital Land and Keppel Corp ) are also mostly depending on property market outside SGP to prosper. It is really challenging for SGP Inc companies if they just depending on our much smaller domestic market unless they venture into overseas markets, but of course with much geopolitical risk like what SING TEL is facing. STI is now basically depending on Banks and REITs to hold it's glory.

Congrats !! to your early retirement and exceptional good performance during this COVID 19 pandemic, I have much to learn from you !!

Yes and sure ! definitely is great idea to have "kopi session " post COVID 19 quarantine when things return to normal...

Cheers !!

Dear STE,

DeleteI have much to learn from you instead. The market that you choose to participate is a difficult one and your proven and excellent track record is something I'll never be able to replicate in the long term if I invest in Singapore. I'm sure your portfolio will come out strong when we get through Covit19.

Best of luck, good health and stay safe!!

Dear av,

DeleteThank you for your kind words and encouragement , I hope we all will come out strong when Covid19 pandemic is over.

You too , stay safe and stay healthy !

Cheers !! :D

Hi there.

ReplyDeleteSorry to hear about the heavy losses on Eagle and ARA US. I kena this sort of sucker punch as well, some companies just melted and became a totally different monster after i bought, big losses for me as well...

Just curious, why did you cut ARA US?

Stay safe and healthy!

Hi Everycetscounts,

DeleteThanks for the comments, yes, losing money is part and partial of investing , hence, position sizing is important. As mentioned in my blog post, I have too much (over confidence ) in REITs backed by hard asset , but some asset's valuation just collapse during crisis , like hospitality during this COVID pandemic , also like Tuas Spring in Hyflux! it suddenly became "zero" when PUB took over but few years back still worth hundreds of millions in their book.

It it really " value in the eyes of be lovers "....

As fro ARA HT , I know they are operation in slight different business model , and also back by stronger sponsor, but I just want to avoid any hospitality REIT at this moment. I know I may miss the up trend once COVID pandemic situation change ( like airlines and transportation stocks , but I just want to have "peace of mind" at this moment as this COVID pandemic is totally new to us...as compared to previous few "financial" related crisis.

You too, stay safe and stay healthy !!

Cheers!! :D

Hi STE,

ReplyDeleteA long time lurker, I tried to workout my excel but to no good result came from it :(

Mind sharing some of your wisdom :|

And stay safe :D

Hi , thanks for contacting , you may please send an email to this e-mail address ( stesg50@gmail.com) , I can forward the sample file on how to plot these charts with some explanations.

DeleteCheers ! :D

Hi STE.

ReplyDeleteI hope you're well. I have been reading your blog since you started writing and I happened to re-read this post. I must say you have really solid grasp of the economy when you wrote

"I think this will continue for quite some time and we may expect even bank to trim their dividend in coming quarters"

I had thought, with the high CET ratios, banks would continue to maintain payouts. haha. But I was wrong and you are right.

Anyways, just want to drop a note to say i love to read what you write and look forward to your next post. 3rd Q dividends perhaps?

Cheers. Stay safe, stay healthy.

Hi The passive Investor,

DeleteThanks for the comments. Hahaha, just lucky for me to make such statement on bank cutting dividend as most of companies are trying to conserve more cash.

Yah, as you pointed out , MAS is setting much higher CET and Tier1 for SG bank and we are more conservative in capital requirement, which is good for investors in the long run , I think.

We have seen so many bank collapsed in western countries and is good to have a prudent approach on capital requirement. Also , I think the cutting of dividend is good for bank and investors in the long run under current challenging economic environment. Although we can say SG banks is still safe but I think is good to be conservative at this point of time,looking at the news of Genting Hong Kong today...

everything is possible ...even privatization of SIA by Temasek if things getting worse.

Yah,, let's stay safe and stay healthy...

Cheers !!

Dear STE

ReplyDeleteI have been a silent reader of your blog for quite some time and I want to commend you (as well as a few of the local bloggers) for contributing much to my education as an investor.

I have been considering diversifying my assets into the foreign stock markets (mainly HK and US markets) for some time. However, what has been stopping me from doing that is that there is no CDP equivalent for the holding of foreign shares. I am a little apprehensive (perhaps due to my ignorance) that my broker is the custodian of my shares and the ownership of the shares is not registered under my name directly.

I am thinking of using FSMOne as my broker. However, despite being regulated by MAS, I am concerned that if the broker goes bust, my share ownership would go down with it (case of MF global). May I ask whether you have the same concern at any point in time prior to invest in foreign share markets? If you do, what convinced you that it is safe for our broker to act as the custodian of our shares? Is there anything I can do to monitor my broker to make sure they are financially sound?

Hi Nigel,

DeleteI guess there is no other options or alternative other than custodian acct if we wanted to diversify into overseas market. As for your concern about broker goes burst and the "counter-party " risk involve , some are think of just using brokerage who have Bank as "ah kong " to back up in case anything happens like DBS or Standard Charted ..

I guess the risk is still there ... is just " heng shui" if the one we choose goes burst , but I would assume the share which being held under "trustee account" should be safe.

Cheers !